After Russia’s invasion of Ukraine, the European Union moved with unprecedented speed to reduce its dependence on Russian pipeline gas. Within a few years, imports were dramatically restructured, infrastructure expanded, and new suppliers secured. Politically, this shift was framed as a success story of energy independence. But independence from whom — and at what cost?

As the EU increasingly relies on liquefied natural gas (LNG), particularly from the United States, a critical question emerges: has Europe reduced its fossil dependency, or merely redirected it?

From Russian pipelines to American tankers

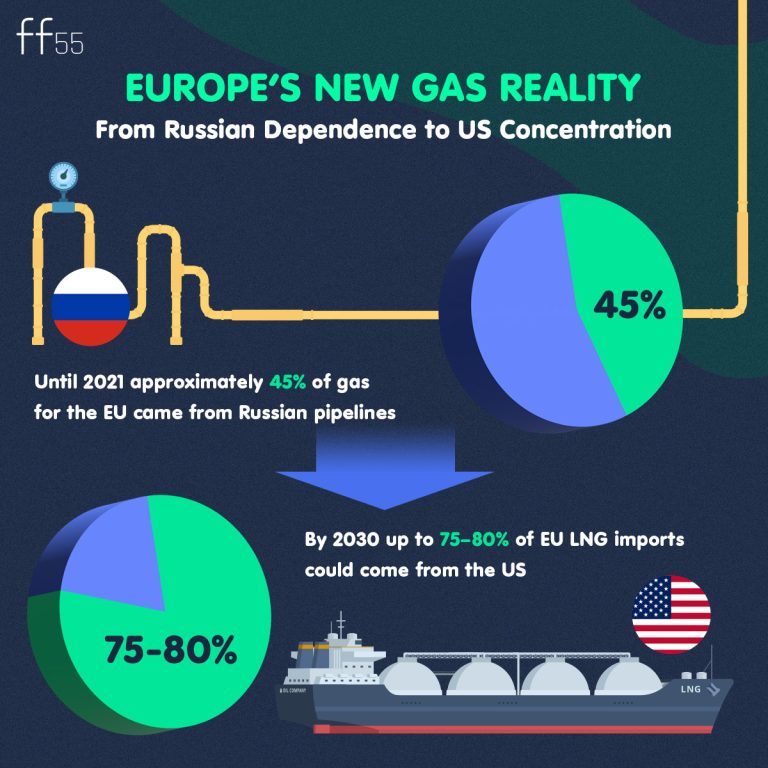

The replacement of Russian gas was not primarily a reduction in fossil fuel consumption. It was a change in source. By 2030, IEEFA estimates that as much as 75-80% of the EU’s LNG imports could originate from the United States, creating a new concentration risk in the supply structure. (Source: IEEFA)

Politico has also reported on Europe’s rapidly increasing dependence on US gas imports following the Russian supply cut-offs. (Source: Politico).

Diversification is often presented as resilience. Yet when imports become heavily concentrated in a single country, the logic of dependency does not disappear: it evolves.

The climate contradiction

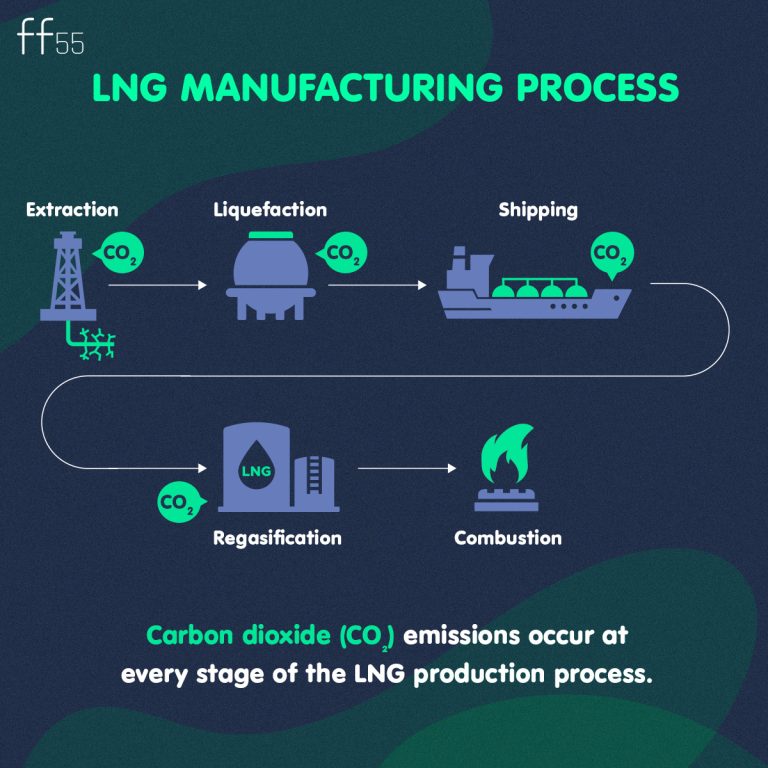

LNG is frequently described as a “transition fuel.” Compared to coal, natural gas emits less CO₂ at the point of combustion. However, this comparison tells only part of the story.

The full lifecycle emissions of LNG include methane leakage during extraction, energy-intensive liquefaction processes, maritime transport and regasification. Environmental organisations and climate researchers have repeatedly warned that replacing Russian gas with US LNG does not necessarily align with EU climate targets. (Source: Greenpeace)

Methane, in particular, has a significantly higher short-term global warming potential than CO₂, which complicates the narrative of LNG as a low-carbon bridge fuel.

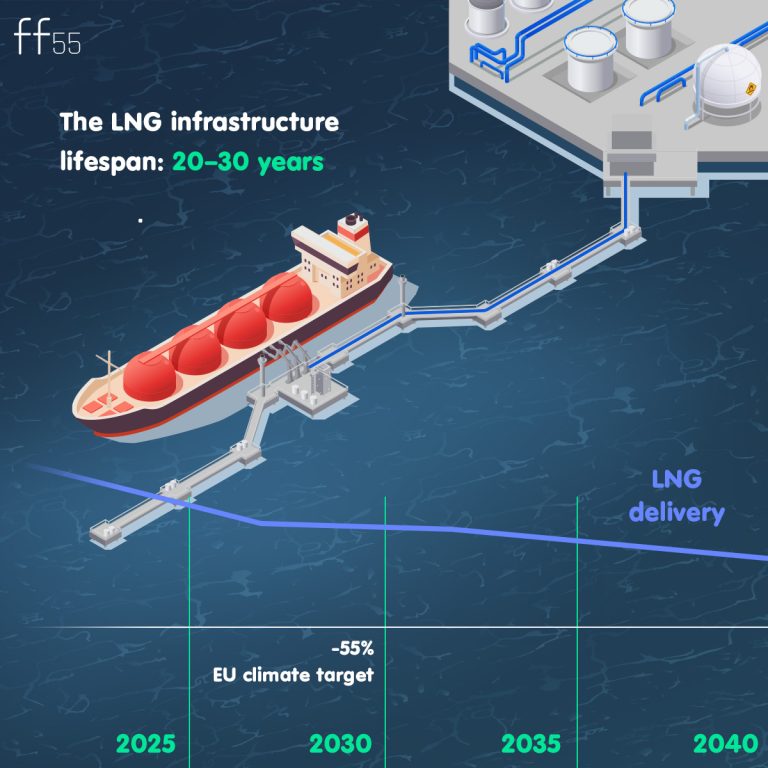

When lifecycle impacts are taken into account, the climate advantage of LNG narrows considerably. This creates a tension within the EU’s climate strategy: while the Fit for 55 agenda aims to reduce greenhouse gas emissions by at least 55% by 2030, expanding LNG infrastructure risks locking in fossil fuel use beyond the transition window.

Long-term contracts and fossil lock-in

eyond physical infrastructure, contractual commitments matter. In 2025, the EU and the United States strengthened their energy cooperation framework, with discussions and agreements extending toward 2028 and beyond. According to a report by Reuters, EU countries have formally approved measures to eliminate Russian gas imports, further solidifying the pivot toward alternative suppliers. (Source: Reuters)

Long-term LNG purchase agreements provide short-term security, but they also create economic incentives to maintain high import volumes. Infrastructure such as LNG terminals and regasification facilities are capital-intensive and typically designed for decades of operation.

This dynamic raises an uncomfortable possibility: what begins as an emergency solution may become structurally embedded in the European energy system.

A new geopolitical exposure

Energy dependency is never purely economic. It is geopolitical. IEEFA has warned that heavy reliance on a single LNG supplier could expose the EU to future political and trade risks. (Source: Riviera / IEEFA)

While the shift from Russia to the United States reduces exposure to one strategic rival, it increases reliance on another major global power whose political direction can shift. Energy exports have historically functioned as instruments of influence.

If supply becomes highly concentrated, political volatility can once again translate into energy uncertainty.

What does this mean for Fit for 55?

The Fit for 55 package was designed to accelerate decarbonisation across sectors. Its logic is clear: structural emission reductions, electrification, renewable expansion and efficiency improvements.

If LNG becomes more than a temporary bridge, it risks conflicting with this trajectory. Investments in fossil infrastructure compete with investments in renewable capacity, storage and grid modernisation. Capital allocation shapes the speed of transition.

The key issue is not whether LNG had a role in stabilising Europe’s energy system after 2022. It likely did. The question is whether that role remains transitional — or whether it gradually becomes entrenched.

Conclusion: Transition or transformation?

The EU’s rapid exit from Russian gas was a geopolitical necessity. Yet replacing one concentrated fossil dependency with another does not automatically constitute systemic transformation.

True energy independence requires more than supplier substitution. It requires reducing exposure to fossil fuels altogether. As Europe advances its climate objectives, the central challenge will be ensuring that emergency solutions do not redefine the long-term direction of the energy system.

Is American LNG a bridge to climate neutrality, or a well-marketed detour?